Petroleum Coke Market Size, Share And Forecast Report 2033

Petroleum Coke Market Size and Outlook 2025 to 2033

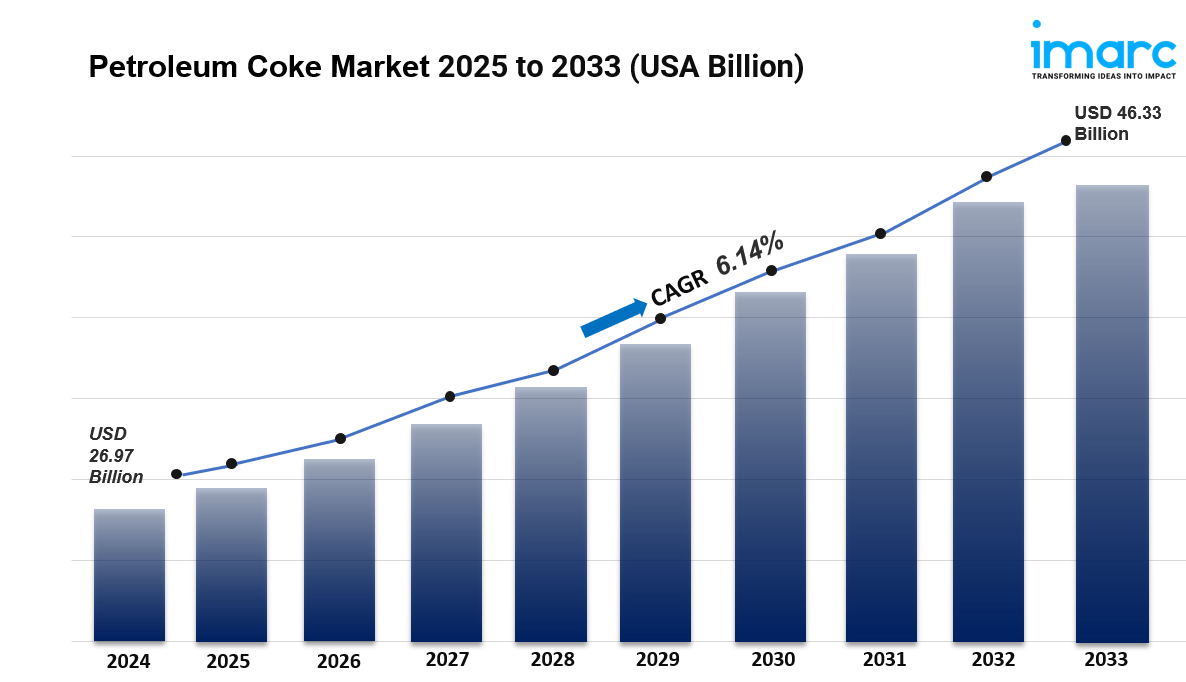

The global petroleum coke market size was valued at USD 26.97 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 46.33 Billion by 2033, exhibiting a growth rate of 6.14% during 2025-2033. North America currently leads the market with over 41.2% share, driven by advanced refining infrastructure, strong industrial demand, and established supply chain networks. The market is experiencing steady growth driven by increasing cement production activities, rising power generation requirements, expanding steel and aluminum manufacturing, and growing demand for high-energy fuel alternatives in industrial applications.

Key Stats for Petroleum Coke Market:

- Petroleum Coke Market Value (2024): USD 26.97 Billion

- Petroleum Coke Market Value (2033): USD 46.33 Billion

- Petroleum Coke Market Forecast Growth Rate: 6.14%

- Leading Segment in Petroleum Coke Market in 2024: Fuel Grade Coke (50.9%)

- Key Regions in Petroleum Coke Market: North America, Asia Pacific, Europe, Latin America, Middle East and Africa

- Top companies in Petroleum Coke Market: BP Plc, Chevron Corporation, Essar Oil Ltd., ExxonMobil Corporation, HPCL-Mittal Energy Limited, Indian Oil Corporation Limited, Reliance Industries Limited, Royal Dutch Shell Plc, Saudi Arabian Oil Co., Valero Energy Corporation, Phillips 66, Marathon Petroleum Corporation.

Request for a sample copy of this report: https://www.imarcgroup.com/petroleum-coke-market/requestsample

Why is the Petroleum Coke Market Growing?

The petroleum coke market is experiencing robust growth as industries worldwide seek cost-effective, high-energy fuel alternatives for their operations. Cement manufacturers have emerged as the largest consumers, accounting for 38.4% of market demand, as petcoke offers exceptional heating value at significantly lower costs compared to traditional coal and natural gas alternatives.

Global infrastructure development drives substantial cement demand, with emerging economies investing trillions in construction projects, roads, bridges, and urban development initiatives. This construction boom directly translates to increased petcoke consumption, as cement plants require reliable, high-calorific fuel sources to maintain production efficiency and cost competitiveness.

Power generation facilities increasingly adopt petcoke as a fuel source, particularly in regions where energy costs significantly impact operational expenses. The material's high carbon content and superior heating value make it an attractive option for utilities seeking to optimize fuel procurement budgets while maintaining reliable electricity generation capacity.

Steel and aluminum industries also contribute to growing demand, using calcined petroleum coke in their production processes. These sectors benefit from petcoke's consistent quality and chemical properties, which are essential for maintaining product specifications and manufacturing efficiency in metallurgical applications.

AI Impact on the Petroleum Coke Market:

Artificial intelligence is transforming the petroleum coke industry by optimizing production processes, quality control, and supply chain management across the entire value chain. AI-powered monitoring systems analyze real-time data from refining operations to predict petcoke yield and quality characteristics, enabling refiners to adjust processing parameters for optimal output.

Machine learning algorithms process vast datasets from multiple refinery operations to identify patterns that improve coking unit efficiency and reduce energy consumption. These systems can predict equipment maintenance needs, preventing costly unplanned shutdowns and ensuring consistent petcoke production schedules that meet customer delivery requirements.

Quality assessment benefits from computer vision technology that automatically analyzes petcoke samples for consistency, contamination, and specifications compliance. This automation reduces testing time from hours to minutes while improving accuracy and reducing human error in quality control processes.

Supply chain optimization powered by AI helps distributors and end-users forecast demand patterns, optimize inventory levels, and coordinate transportation logistics. Predictive analytics enable better planning for seasonal demand fluctuations and help companies maintain adequate supply while minimizing storage costs and working capital requirements.

Segmental Analysis:

Analysis by Type:

- Fuel Grade Coke

- Calcined Coke

Fuel grade coke dominates the market with 50.9% share in 2024, serving primarily as a high-energy fuel for power plants, cement kilns, and industrial boilers. This segment benefits from petcoke's superior calorific value and cost-effectiveness compared to traditional fossil fuels.

Analysis by Application:

- Power Plants

- Cement Kilns

- Steel

- Aluminum

- Fertilizer

- Others

Cement kilns represent the largest application segment with 38.4% market share, driven by extensive infrastructure development projects and construction activities worldwide. The cement industry values petcoke for its consistent heat generation and cost advantages over alternative fuels.

Analysis by End-User:

- Industrial

- Commercial

- Utilities

Industrial end-users account for the majority of petcoke consumption, utilizing the material in manufacturing processes requiring high-temperature heating and energy-intensive operations across various sectors including metals, chemicals, and building materials.

Analysis of Petroleum Coke Market by Regions

- North America

- Asia Pacific

- Europe

- Latin America

- Middle East and Africa

North America leads the global market with over 41.2% share, supported by extensive refining capacity, advanced petrochemical infrastructure, and strong domestic demand from cement, power generation, and industrial sectors that require reliable, cost-effective fuel sources.

Speak To An Analyst: https://www.imarcgroup.com/request?type=report&id=2592&flag=C

What are the Drivers, Restraints, and Key Trends of the Petroleum Coke Market?

Market Drivers:

Global cement production expansion drives substantial petcoke demand, with developing nations investing heavily in infrastructure projects requiring massive quantities of cement. Construction spending exceeds $10 trillion globally, creating sustained demand for cost-effective, high-energy fuels in cement manufacturing operations.

Power generation requirements in emerging economies fuel petcoke adoption as utilities seek affordable alternatives to expensive imported coal and natural gas. Countries with growing electricity demand but limited domestic fuel resources find petcoke attractive for baseload power generation due to its competitive pricing and reliable supply availability.

Steel and aluminum production growth supports calcined petroleum coke demand, as these industries require consistent, high-quality carbon materials for metallurgical processes. Global steel production exceeds 1.8 billion tons annually, requiring substantial quantities of specialized carbon additives that petcoke provides.

Industrial energy cost optimization pressures encourage manufacturers to seek fuel alternatives that reduce operational expenses without compromising production efficiency. Petcoke's superior heating value per dollar makes it attractive for energy-intensive industries seeking to maintain competitiveness in global markets.

Market Restraints:

Environmental regulations and emission standards create compliance challenges for petcoke users, particularly in developed markets where air quality regulations limit sulfur content and particulate emissions. Stricter environmental policies may restrict petcoke usage in certain applications or require expensive emission control equipment.

Transportation and handling complexities affect market accessibility, as petcoke requires specialized storage facilities and handling equipment to prevent dust emissions and maintain product quality. Logistics costs can significantly impact delivered pricing, particularly for inland locations distant from refineries.

Alternative fuel competition intensifies as renewable energy costs decline and natural gas availability increases in some regions. Competitive pricing from alternative energy sources may limit petcoke adoption in price-sensitive applications, particularly in power generation sectors.

Quality variability concerns affect customer confidence, as petcoke specifications can vary depending on crude oil sources and refining processes. Inconsistent quality may require additional processing or blending to meet end-user specifications, increasing handling costs and complexity.

Market Key Trends:

Sustainability initiatives drive development of cleaner petcoke processing technologies and emission control systems that reduce environmental impact while maintaining cost advantages. Industry investments in advanced combustion technologies and pollution control equipment enable continued petcoke usage under stricter environmental regulations.

Quality standardization efforts improve market transparency and customer confidence through established grading systems and specification standards. Industry associations develop unified quality metrics that facilitate trading and enable better matching of petcoke grades to specific application requirements.

Supply chain optimization utilizes digital technologies to improve logistics efficiency, reduce transportation costs, and enhance delivery reliability. Advanced tracking systems and predictive analytics help suppliers and customers optimize inventory management and reduce supply chain disruptions.

Regional market integration expands through improved transportation infrastructure and trade relationships that connect petcoke producers with global markets. Enhanced port facilities and shipping capabilities enable more efficient international trade and market access for both suppliers and buyers.

Leading Players of Petroleum Coke Market:

According to IMARC Group's latest analysis, prominent companies shaping the global Petroleum Coke landscape include:

- BP Plc

- Chevron Corporation

- Essar Oil Ltd.

- ExxonMobil Corporation

- HPCL-Mittal Energy Limited

- Indian Oil Corporation Limited

- Reliance Industries Limited

- Royal Dutch Shell Plc

- Saudi Arabian Oil Co.

- Valero Energy Corporation

- Phillips 66

- Marathon Petroleum Corporation

- ConocoPhillips

- TotalEnergies SE

These leading providers are expanding their footprint through strategic partnerships, refining capacity optimization, and advanced production technologies to meet growing industrial demand for reliable, cost-effective fuel solutions across cement, power generation, steel, aluminum, and other energy-intensive manufacturing sectors.

Key Developments in Petroleum Coke Market:

- January 2025: Major petroleum refiners announced capacity expansions for coking units to meet growing industrial demand, with billions invested in advanced processing technologies that improve petcoke quality and yield from crude oil refining operations.

- December 2024: Leading petcoke suppliers implemented AI-powered quality control systems that enhance product consistency and reduce variability, enabling better matching of petcoke grades to specific customer requirements across various industrial applications.

- November 2024: Strategic partnerships formed between refining companies and cement manufacturers to establish long-term supply agreements, ensuring reliable petcoke availability for critical industrial operations while optimizing logistics and reducing transportation costs.

- October 2024: Environmental technology developments introduced advanced emission control systems for petcoke combustion, enabling continued usage in regions with strict air quality regulations while maintaining cost advantages over alternative fuels.

- September 2024: Infrastructure investments in specialized petcoke handling and storage facilities improved supply chain efficiency, reducing logistics costs and enabling better service to industrial customers requiring consistent, high-quality fuel delivery.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services.

IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302