Mono Material Barrier Packaging Market Outlook: Growth, Demand & Future Opportunities

Mono Material Barrier Packaging Market Overview

The mono-material barrier packaging market is experiencing significant growth as industries increasingly adopt recyclable and sustainable packaging solutions. Rising environmental awareness, stringent regulations, and corporate sustainability commitments are accelerating the transition from conventional multi-layer packaging to mono-material alternatives. These packaging solutions are manufactured using a single polymer, such as polyethylene (PE) or polypropylene (PP), while maintaining strong barrier protection against oxygen, moisture, and contaminants.

Request Sample Link:

https://packagingmarketinsights.com/report/mono-material-barrier-packaging-market/request-sample

Mono material barrier packaging simplifies recycling processes, improves material recovery rates, and supports circular economy initiatives. Growing adoption across the food & beverage, pharmaceutical, and personal care industries, combined with continuous innovation in barrier technologies, is expected to sustain market expansion throughout the forecast period.

Market Size and Forecast

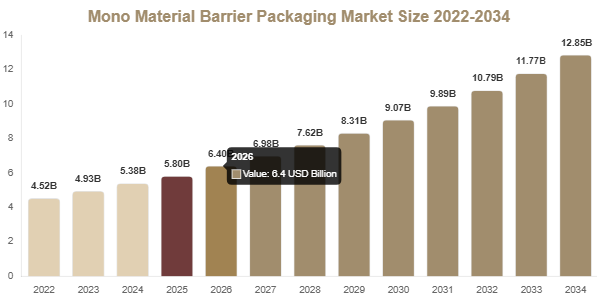

The mono-material barrier packaging market was valued at USD 5.8 billion in 2025 and is estimated to reach USD 6.4 billion in 2026. According to Packaging Market Insights, the market is projected to achieve approximately USD 13.9 billion by 2034, expanding at a CAGR of 9.1% during the forecast period.

The impressive growth outlook is supported by increasing demand for recyclable packaging solutions, technological advancements in barrier materials, and the growing emphasis on reducing packaging complexity. As governments introduce stricter recycling regulations and brands commit to sustainable packaging goals, mono-material barrier packaging continues to gain widespread acceptance across multiple industries.

Market Drivers

Increasing Regulatory Pressure for Sustainable Packaging

Government regulations aimed at reducing plastic waste are playing a major role in driving the mono-material barrier packaging market. Regulatory frameworks across Europe and North America encourage recyclable packaging while discouraging the use of complex multi-layer materials. These initiatives motivate manufacturers to invest in mono-material solutions that comply with evolving environmental standards.

Growing Consumer Preference for Eco-Friendly Packaging

Consumers are increasingly choosing products packaged in sustainable and recyclable materials. This shift in purchasing behavior has encouraged companies in food & beverage, pharmaceuticals, and personal care to adopt mono-material barrier packaging as part of their sustainability strategies. Packaging has become an important factor in purchasing decisions, making environmentally responsible solutions increasingly valuable.

Technological Advancements in Barrier Materials

Continuous innovation in advanced coatings, plasma treatments, and nanotechnology is improving the performance of mono-material packaging. These developments enable manufacturers to deliver enhanced oxygen and moisture barriers while preserving recyclability, increasing adoption across industries requiring high-performance packaging.

Market Challenges

Performance Limitations Compared to Multi-Layer Packaging

Although mono-material barrier packaging offers substantial sustainability benefits, it still faces challenges in matching the barrier performance of traditional multi-layer packaging structures. Applications requiring extended shelf life or superior protection against harsh environmental conditions may continue relying on multi-layer solutions.

Higher Cost of Advanced Barrier Technologies

Achieving barrier performance comparable to conventional packaging often requires specialized coatings and advanced treatments, increasing production costs. This balance between sustainability, performance, and affordability remains a key challenge, particularly in price-sensitive markets where manufacturers carefully evaluate production expenses before transitioning to mono-material solutions.

Market Opportunities

Expansion Across Emerging Economies

Emerging markets present considerable growth opportunities for the mono-material barrier packaging market. Rapid urbanization, increasing disposable incomes, expanding retail sectors, and growing demand for packaged products are encouraging the adoption of sustainable packaging solutions throughout Asia Pacific and Latin America.

Innovation in High-Barrier Mono Materials

Ongoing research in polymer science and barrier technology is creating new opportunities for high-performance mono-material packaging. Advances in nanotechnology and innovative coating techniques are enabling manufacturers to produce recyclable films with improved oxygen and moisture resistance. These innovations are expected to expand applications across pharmaceutical and premium food packaging.

Market Segmentation

By Material Type

Polyethylene (PE) dominated the market in 2024, accounting for approximately 48% of the market share. Its flexibility, durability, moisture resistance, and compatibility with existing recycling systems make it the preferred material for sustainable packaging.

Polypropylene (PP) is projected to register the fastest CAGR of 10.2% during the forecast period due to its superior heat resistance and mechanical strength, particularly for pharmaceutical and personal care applications.

Material segments include the following:

-

Polyethylene (PE)

-

Polypropylene (PP)

-

Others

By Application

The Food & Beverage segment accounted for approximately 52% of the market share in 2024 due to strong demand for packaging that preserves freshness while supporting sustainability objectives.

The pharmaceutical segment is expected to grow at the fastest CAGR of 9.8% during the forecast period as innovations enable mono-material packaging to meet strict healthcare packaging requirements.

Application segments include:

-

Food & Beverage

-

Pharmaceuticals

-

Personal Care

-

Others

By End-Use Industry

Food processing led the market in 2024 with approximately 46% market share, supported by rising global demand for packaged food products.

The E-commerce segment is anticipated to record the fastest CAGR of 10.8% through 2034, driven by increasing online retail activity and demand for lightweight, recyclable packaging.

End-use industries include:

-

Food Processing

-

Healthcare

-

E-commerce

-

Retail

Regional Analysis

North America

North America represented approximately 28% of the global market share in 2025 and is expected to grow at a CAGR of 8.7% through 2034. Strong recycling infrastructure, regulatory support, and investments in sustainable packaging technologies continue to strengthen regional growth. The United States remains the leading contributor due to its advanced packaging industry and widespread adoption of recyclable packaging.

Europe

Europe accounted for around 30% of the global market in 2025 and is forecast to expand at a CAGR of 9.3%. Stringent environmental regulations and circular economy initiatives are accelerating the transition toward mono-material packaging. Germany leads regional growth through its strong manufacturing capabilities and implementation of extended producer responsibility programs.

Asia Pacific

Asia Pacific held approximately 25% of the market share in 2025 and is projected to achieve the fastest CAGR of 10.5% through 2034. Rapid industrialization, urbanization, expanding retail industries, and increasing government efforts to reduce plastic waste are driving substantial market opportunities. China remains the dominant regional market.

Middle East & Africa

The Middle East & Africa accounted for around 9% of the global market share in 2025 and is expected to grow at a CAGR of 8.2%. Investments in industrial development and growing awareness regarding sustainable packaging continue to support regional market expansion, with the United Arab Emirates leading adoption.

Latin America

Latin America represented approximately 8% of the global market in 2025 and is forecast to expand at a CAGR of 8.9%. Growing demand for packaged food and beverages, combined with increasing environmental awareness, is supporting the adoption of recyclable monomaterial packaging. Brazil remains the largest regional market.

Key Players

The mono-material barrier packaging market remains moderately competitive as manufacturers continue investing in product innovation, sustainability initiatives, and geographical expansion. Key market participants include the following:

-

Amcor Plc

-

Berry Global Inc.

-

Mondi Group

-

Sealed Air Corporation

-

Sonoco Products Company

-

Huhtamaki Oyj

-

Coveris Holdings S.A.

-

Constantia Flexibles

These companies are strengthening their market positions through research and development, advanced barrier technologies, strategic collaborations, mergers, acquisitions, and expanded sustainable packaging portfolios.

Conclusion

The mono-material barrier packaging market is positioned for strong long-term growth, supported by increasing regulatory requirements, rising consumer preference for recyclable packaging, and continuous innovation in barrier technologies. The transition toward mono-material packaging reflects the packaging industry's broader commitment to sustainability, circular economy principles, and improved recycling efficiency.

Report Link:

https://packagingmarketinsights.com/report/mono-material-barrier-packaging-market

With the market expected to grow from USD 5.8 billion in 2025 to USD 13.9 billion by 2034 at a CAGR of 9.1%, monomaterial barrier packaging is becoming an increasingly important solution across food & beverage, pharmaceutical, personal care, and e-commerce applications. Continued technological advancements and expanding opportunities in emerging economies are expected to further accelerate market adoption throughout the forecast period.