Glass Wings Rising: Aerospace Fiberglass Market on Track for Strong Growth Through 2032

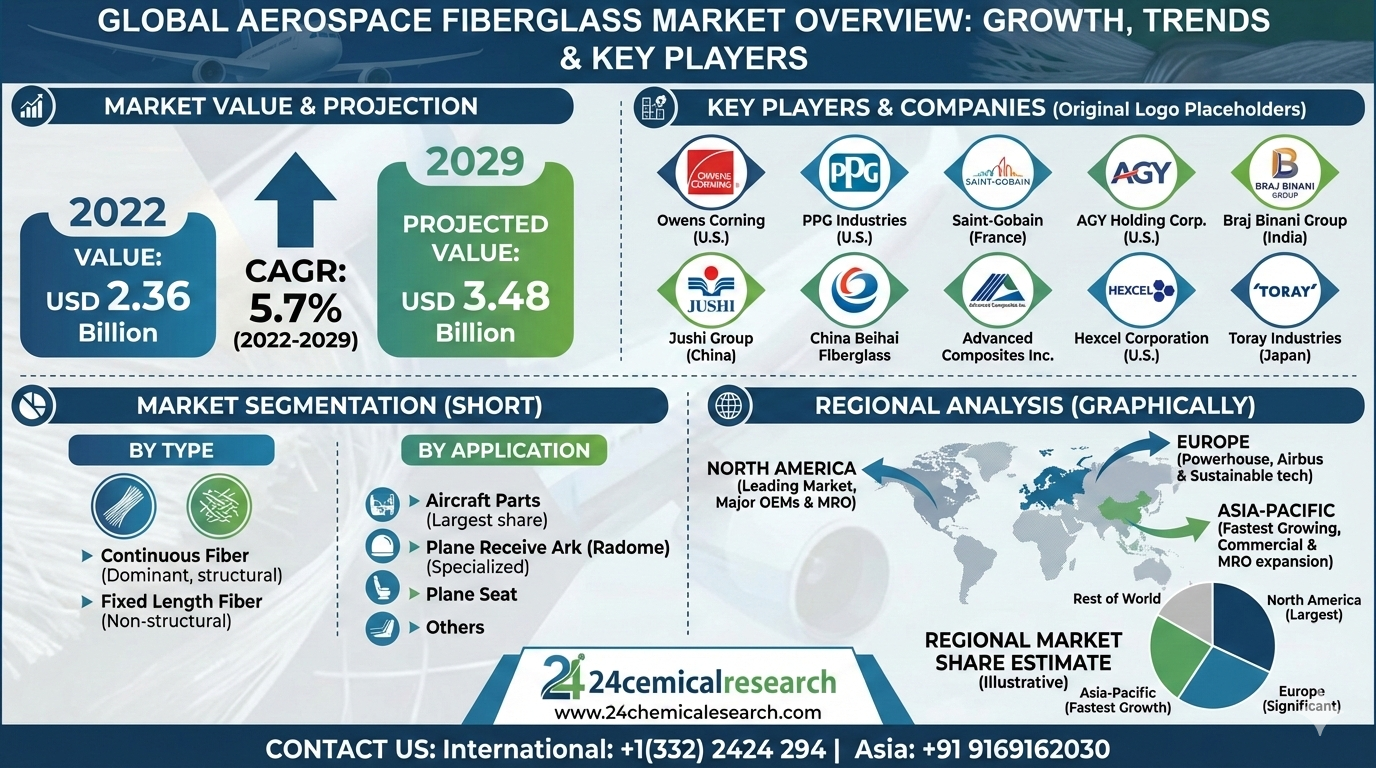

Global Aerospace Fiberglass market was valued at USD 2.36 billion in 2022 and is projected to reach USD 3.48 billion by 2029, exhibiting a steady CAGR of 5.7% during the forecast period.

Aerospace fiberglass, a composite material primarily composed of fine glass fibers embedded in a polymer resin matrix, has long been a fundamental material in aircraft construction. Its journey from early radomes and secondary structures to critical primary components in modern aircraft underscores its enduring value. The material's outstanding properties—including an exceptional strength-to-weight ratio, excellent corrosion resistance, and remarkable dielectric properties—make it indispensable for reducing overall aircraft weight, enhancing fuel efficiency, and ensuring reliable performance in demanding flight conditions. Unlike metallic alternatives, fiberglass is non-conductive and immune to galvanic corrosion, which simplifies design and extends service life in harsh environments.

Get Full Report Here: https://www.24chemicalresearch.com/reports/241792/global-aerospace-fiberglass-forecast-market-2023-2032-48

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Surging Demand for Fuel-Efficient Aircraft: The relentless pressure to reduce operational costs and meet stringent environmental regulations is the most potent driver for aerospace fiberglass. Every 1% reduction in aircraft weight translates to approximately a 0.75% savings in fuel consumption. With jet fuel constituting 20-30% of an airline's operating expenses, the economic incentive for lightweighting is enormous. Fiberglass composites enable weight reductions of 20-30% compared to traditional aluminum structures in non-primary components like fairings, interiors, and radomes. This driver is amplified by the global commercial aircraft fleet, which is projected to nearly double over the next two decades, creating sustained demand for new, more efficient airframes.

- Expansion of the Global MRO (Maintenance, Repair, and Overhaul) Sector: The massive installed base of aircraft, which includes thousands of planes utilizing fiberglass components, creates a robust aftermarket. The global aerospace MRO market is a colossal sector, expected to exceed $110 billion annually. Fiberglass parts are subject to wear, environmental degradation, and accidental damage, requiring regular inspection, repair, and replacement. Furthermore, cabin interior refurbishment cycles, which occur every 5-7 years for most commercial aircraft, heavily rely on fiberglass for sidewalls, stowage bins, and ceiling panels, providing a recurring revenue stream independent of new aircraft production rates.

- Technological Advancements in Material Formulations: The industry is far from stagnant. Continuous innovation in fiber sizing, resin chemistry, and manufacturing processes is enhancing the performance envelope of aerospace fiberglass. The development of S-3 glass fibers, for instance, offers tensile strength improvements of 30-40% over traditional E-glass. Similarly, advancements in high-performance thermoset and thermoplastic resins are improving damage tolerance, fire resistance (meeting stringent FAR 25.853 standards), and overall durability. These innovations are opening doors for fiberglass in more demanding applications, effectively expanding its market share within the airframe.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/241792/global-aerospace-fiberglass-forecast-market-2023-2032-48

Significant Market Restraints Challenging Adoption

Despite its established role, the market faces hurdles that influence material selection decisions.

- Intense Competition from Advanced Composites: The rise of carbon fiber reinforced polymers (CFRP) represents the most significant competitive threat. CFRP offers a superior strength-to-weight ratio and stiffness, making it the material of choice for primary structures like wings and fuselages in next-generation aircraft (e.g., Boeing 787, Airbus A350). While fiberglass maintains a cost advantage of 40-60% over carbon fiber, the performance gap has constrained its growth in high-load-bearing applications. This has effectively relegated a significant portion of the market to secondary structures and interior applications, where its properties are more than adequate.

- Stringent and Evolving Certification Requirements: The aerospace industry is governed by the world's most rigorous certification standards from authorities like the FAA and EASA. Qualifying a new fiberglass material or process for use on an aircraft is a painstakingly slow and expensive endeavor, often taking several years and costing millions of dollars. Any minor change in the supply chain, such as a new resin supplier or a modification to the fiber manufacturing process, can trigger a requalification effort. This regulatory inertia can slow down the adoption of innovative, cost-saving material solutions and favors incumbent, already-qualified materials.

Critical Market Challenges Requiring Innovation

The industry faces ongoing challenges in manufacturing and sustainability that demand continuous improvement.

Manufacturing complex, large-scale fiberglass components with the required precision and repeatability remains a challenge. Achieving void content consistently below 2% in large hand-layup or resin infusion parts is difficult, and automated fiber placement (AFP) technologies, commonplace with carbon fiber, are less developed for fiberglass applications. This can lead to higher scrap rates and labor costs, impacting the overall economics. Furthermore, the industry is grappling with the environmental footprint of thermoset composites. The majority of aerospace fiberglass uses epoxy resins that are not easily recyclable, leading to end-of-life challenges. While thermal and chemical recycling methods are under development, a cost-effective, scalable circular economy model for cured aerospace fiberglass composites remains elusive, presenting a significant long-term challenge.

Additionally, the market is susceptible to volatility in raw material inputs. The production of glass fibers is energy-intensive, and fluctuations in natural gas and electricity prices can directly impact manufacturing costs. Similarly, the petrochemical-based epoxy resins are subject to the price volatility of their feedstocks. This creates budgeting challenges for both material suppliers and aerospace OEMs, who operate on long-term contracts with fixed pricing.

Vast Market Opportunities on the Horizon

- Growth of the Urban Air Mobility (UAM) and Unmanned Aerial Vehicle (UAV) Sectors: The emerging eVTOL (electric Vertical Take-Off and Landing) and commercial drone markets represent a massive new frontier. These aircraft have stringent weight requirements for battery efficiency and payload capacity but often operate at lower stresses than commercial jets. This creates a perfect application for cost-effective, lightweight fiberglass composites for airframes, rotor blades, and housings. The projected market for UAM is expected to grow exponentially over the next decade, offering a substantial new addressable market for aerospace fiberglass suppliers.

- Advancements in Sustainable and "Greener" Composites: There is a growing push within aerospace for sustainable materials. This is driving R&D into bio-based epoxy resins and recyclable thermoplastic fiberglass composites. Companies that can successfully develop and certify "green" fiberglass solutions that meet performance requirements will gain a significant competitive advantage, especially as airlines and OEMs make public commitments to sustainability. Early adopters of these technologies are poised to capture market share as environmental criteria become a larger factor in material selection.

- Strategic Focus on Integrated Solutions and Value-Added Services: The market is seeing a shift from selling raw materials to providing engineered solutions. Leading players are increasingly offering pre-impregnated fabrics (prepregs), tailored kits, and even fully fabricated sub-assemblies. This vertical integration allows them to capture more value and build stronger, more strategic partnerships with OEMs. By reducing the manufacturing complexity and risk for the aircraft manufacturer, suppliers can secure long-term contracts and create higher barriers to entry for competitors.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Continuous Fiber, Fixed Length Fiber, and others. Continuous Fiber dominates the aerospace segment, as it provides the superior mechanical properties—such as high tensile strength and stiffness—required for structural applications like fairings, ducting, and rotor blades. The continuous strands allow for load to be efficiently distributed along the fiber length. Fixed Length Fiber (chopped strand) is used less frequently, primarily in non-structural applications like filler materials or for adding rigidity to certain composite panels.

By Application:

Application segments include Aircraft Parts, Plane Seat, Plane Receive Ark (Radome), and others. The Aircraft Parts segment holds the largest share, encompassing a vast range of components from interior panels and flooring to wing-to-body fairings and engine nacelles. However, the Plane Receive Ark (Radome) application is critically important and highly specialized, as it requires fiberglass formulations with specific dielectric properties to protect radar systems while being transparent to radio waves.

By End-User Industry:

The end-user landscape is primarily divided between Commercial Aviation, Military Aviation, and General Aviation. The Commercial Aviation sector is the largest consumer, driven by high-production rates from Airbus and Boeing and the extensive use of fiberglass in single-aisle and wide-body aircraft interiors and secondary structures. The Military sector demands specialized fiberglass for applications requiring durability and specific performance characteristics, often in lower volumes but at higher margins.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/241792/global-aerospace-fiberglass-forecast-market-2023-2032-48

Competitive Landscape:

The global Aerospace Fiberglass market is moderately consolidated, featuring a mix of large multinational materials corporations and specialized composite suppliers. The top players—Owens Corning (US), PPG Industries (US), and Saint-Gobain (France)—leverage their vast glass fiber production expertise and global reach to serve the aerospace sector. Their dominance is reinforced by long-term supply agreements with major aerospace OEMs and their ability to invest in the stringent quality control and certification processes required by the industry.

List of Key Aerospace Fiberglass Companies Profiled:

- Owens Corning (U.S.)

- PPG Industries (U.S.)

- Saint-Gobain (France)

- AGY Holding Corp. (U.S.)

- Braj Binani Group (India)

- Jushi Group (China)

- China Beihai Fiberglass

- Advanced Composites Inc.

- Hexcel Corporation (U.S.)

- Toray Industries (Japan)

The competitive strategy revolves heavily around technological innovation to improve material performance, rigorous cost control to maintain competitiveness against carbon fiber, and forging deep, collaborative partnerships with aerospace OEMs and tier-one suppliers to integrate fiberglass solutions early in the aircraft design process.

Regional Analysis: A Global Footprint with Distinct Leaders

- North America: Is the leading market, accounting for the largest share globally. This is primarily driven by the presence of aerospace giants Boeing and Lockheed Martin, a massive MRO ecosystem, and strong defense spending. The region's well-established supply chain and focus on technological innovation keep it at the forefront of the market.

- Europe: Represents another powerhouse, anchored by Airbus and a strong network of tier-one suppliers. European companies are also leaders in developing sustainable composite technologies. The region's robust aerospace cluster and collaborative research initiatives, such as those funded by the EU, ensure its continued significance.

- Asia-Pacific: Is the fastest-growing region, fueled by the rapid expansion of commercial aviation in China and India. The establishment of COMAC in China and increasing investments in indigenous aircraft programs are driving domestic demand for aerospace fiberglass. The region is also becoming a major hub for MRO activities, further boosting market growth.

Get Full Report Here: https://www.24chemicalresearch.com/reports/241792/global-aerospace-fiberglass-forecast-market-2023-2032-48

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/241792/global-aerospace-fiberglass-forecast-market-2023-2032-48

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/