TElectrode Binders for Lithium-ion Batteries Market to Reach USD 2.23B by 2034 at 9.3% CAGR

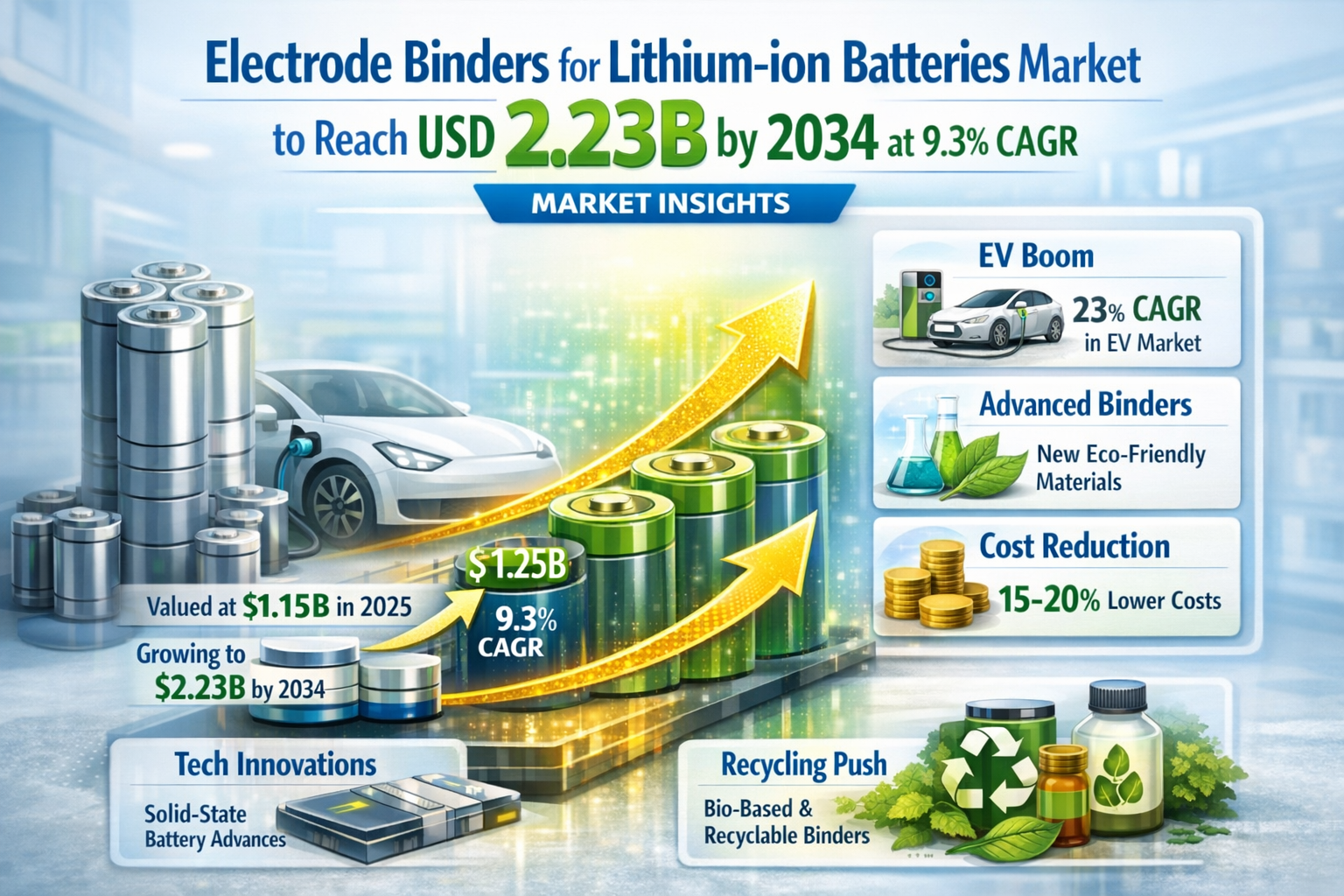

Global electrode binders for lithium-ion batteries market was valued at USD 1,154 million in 2025 and is projected to reach USD 2,231 million by 2034, exhibiting a remarkable CAGR of 9.3% during the forecast period.

Electrode binders are specialized polymer materials that play a critical role in lithium-ion battery manufacturing by binding active materials, conductive additives, and current collectors into cohesive electrode structures. These materials ensure mechanical integrity during charge-discharge cycles while facilitating ion and electron transport, directly impacting battery performance, safety, and cycle life. The market produced approximately 148 kilotons of binders in 2025, with average prices around USD 8,569 per metric ton, reflecting their high-value nature despite small usage volumes per battery.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307085/electrode-binders-for-lithiumion-batteries-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Electric Vehicle Revolution and Energy Storage Demand: The global electric vehicle market's projected 23% CAGR through 2030, coupled with over $515 billion in automaker EV investments, creates unprecedented demand for high-performance lithium-ion batteries. Electrode binders are critical enablers for next-generation batteries requiring enhanced energy density and cycle life. The parallel growth in grid-scale energy storage, projected to expand at 14.2% CAGR through 2034, further accelerates binder demand for large-format battery applications where electrode integrity is paramount.

- Technological Advancements in Binder Formulations: Innovations in water-based binder systems are gaining 12% more market share annually, driven by environmental regulations and performance benefits. These advanced formulations demonstrate superior electrode stability while reducing volatile organic compound emissions by over 90% compared to traditional solvent-based systems. The shift from PVDF to advanced acrylic binders enables 15-20% cost reduction per battery cell while improving thermal stability and processing safety.

- High-Nickel and Silicon Electrode Compatibility: The industry's transition to high-nickel cathodes (Ni-content >80%) and silicon-based anodes requires binders with enhanced elasticity and interfacial properties. Functional binders incorporating polyacrylic acid (PAA) and carboxymethyl cellulose (CMC) chemistries are growing at 12.4% CAGR, enabling accommodation of larger volume changes during cycling while maintaining electrode integrity through 1000+ charge cycles.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307085/electrode-binders-for-lithiumion-batteries-market

Significant Market Restraints Challenging Adoption

Despite its promising growth, the market faces several hurdles that must be overcome for widespread adoption.

- High Switching Costs and Qualification Barriers: Battery manufacturers exhibit strong inertia against binder formulation changes due to extensive qualification processes requiring 2-3 years and costing $2-5 million per new material. This creates significant barriers for novel binder technologies despite their performance advantages, particularly for automotive applications where reliability and safety validation are paramount.

- Raw Material Price Volatility and Supply Chain Complexity: Fluctuations in petroleum-derived binder feedstock prices create unpredictable manufacturing costs, with specialty polymers experiencing 30-40% annual price swings. The immature supply chain faces additional challenges from graphite price volatility (15-25% annually) and increased complexity in transporting and storing binder materials compared to traditional alternatives.

Critical Market Challenges Requiring Innovation

The transition from laboratory development to industrial-scale manufacturing presents substantial technical and economic challenges. Maintaining material consistency at production volumes exceeding 100 metric tons annually proves difficult, with current processes achieving only 60-70% usable output yield. Ensuring dispersion stability in industrial formulations remains problematic, leading to premature aggregation in 30-40% of composite applications. These technical hurdles necessitate R&D investments consuming 15-20% of material firms' revenues, creating high barriers for smaller players.

Regulatory compliance adds another layer of complexity, with differing chemical regulations across markets (REACH, TSCA, etc.) requiring costly regional binder formulations. Compliance testing can add 6-9 months to product launch timelines, particularly challenging for medical device and automotive applications where safety certifications are stringent.

Vast Market Opportunities on the Horizon

- Solid-State Battery Development: Emerging solid-state battery technologies require entirely new binder chemistries compatible with ceramic electrolytes, opening a $1.2 billion addressable market for specialized polymer developers by 2028. Early movers in ceramic-compatible binders are securing strategic partnerships with major battery producers targeting next-generation energy storage solutions.

- Sustainable and Bio-Based Binder Solutions: Plant-derived binders are gaining significant traction, with lignin-based solutions showing particular promise for environmentally conscious applications. The bio-binder segment could capture 18% market share by 2027 as ESG investing criteria increasingly influence procurement decisions across the battery supply chain, particularly in European and North American markets.

- Advanced Functional Binders for Fast-Charging Applications: The growing demand for fast-charging capabilities in electric vehicles and consumer electronics drives need for binders that maintain electrode integrity under rapid lithium-ion intercalation. Innovative formulations incorporating conductive additives and elastic polymers are emerging to address these requirements, particularly for silicon anode applications where volume expansion challenges are most pronounced.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Anode Binders and Cathode Binders. Cathode Binders currently lead the market, driven by technological shifts toward high-nickel formulations requiring specialized binding solutions that maintain structural integrity under extreme operating conditions while preventing harmful side reactions. Anode binders are experiencing rapid innovation, particularly for silicon-based systems where elasticity and adhesion requirements are more demanding.

By Application:

Application segments include Power Batteries, Energy Storage Batteries, Digital Batteries, and others. The Power Battery segment dominates binder requirements due to stringent performance demands in electric vehicles where adhesives must withstand aggressive cycling while maintaining electrode cohesion. Energy storage applications show the fastest growth rate, driven by grid-scale deployments requiring binders that ensure long-term reliability and safety.

By Binder System:

The market is divided into Oil-Based Binders, Water-Based Binders, and Solvent-Free Systems. Water-Based Binders are gaining rapid adoption as environmentally-friendly alternatives to traditional PVDF systems, offering superior processing safety and reduced VOC emissions while facing technical challenges in maintaining performance parity for high-energy density applications.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307085/electrode-binders-for-lithiumion-batteries-market

Competitive Landscape:

The global electrode binders market is characterized by intense competition among established specialty chemical companies with deep materials expertise. The market is semi-consolidated, with the top players accounting for over 60% of global market share through advanced production capabilities and strong partnerships with major battery manufacturers.

List of Key Electrode Binders Companies Profiled:

- Kureha Corporation (Japan)

- Solvay (Belgium)

- ZEON CORPORATION (Japan)

- Arkema (France)

- NIPPON A&L Inc. (Japan)

- JSR Corporation (Japan)

- Zhejiang Fluorine Chemical New Material Co., Ltd. (China)

- LG Chem (South Korea)

- BASF SE (Germany)

- Sichuan Yindile Material Technology Group Co., Ltd. (China)

- Trinseo LLC (United States)

- Shanghai Putailai New Energy Technology Co., Ltd. (China)

The competitive strategy focuses overwhelmingly on R&D to enhance product quality and reduce costs, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate new applications. This approach secures future demand while addressing the specific technical requirements of evolving battery technologies.

Regional Analysis: A Global Footprint with Distinct Leaders

- Asia: Dominates the global market with 78% share, led by China's massive battery manufacturing expansion and strong government support for electric vehicles and energy storage projects. The region benefits from a well-established supply chain, with Asian producers leading the transition to water-based binders while developing formulations for high-nickel cathodes. Japan and South Korea contribute significant specialty chemical expertise for premium battery applications.

- North America: Shows strong growth potential particularly for premium applications in electric vehicles and stationary storage. The region benefits from advanced battery R&D facilities and collaborations between binder manufacturers and automotive OEMs, with environmental regulations accelerating adoption of sustainable binder solutions.

- Europe: Emphasizes environmental sustainability and performance standards, with stringent regulations driving innovation in eco-friendly formulations. European chemical companies focus on specialty binders for high-nickel cathodes and silicon anodes, supported by strong intellectual property protection and cross-value chain collaborations.

- Rest of World: emerging markets show nascent but growing interest, with Southeast Asia developing production capabilities to serve regional battery manufacturing hubs and countries like India building domestic capacity for evolving EV and electronics markets.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307085/electrode-binders-for-lithiumion-batteries-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307085/electrode-binders-for-lithiumion-batteries-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/